My wife is an entrepreneur, and she holds multiple shares in various companies. Since she owned these shares before our marriage, I assume they are not part of our joint ownership of spouses (similar to community property under common law and referred to as BSM in Slovak law). Only the income generated from these shares during our marriage, such as dividends, might be considered part of our joint ownership of spouses. One of my wife’s companies is now taking out a loan, and the bank is requiring shareholders to sign a statement of guarantee. Additionally, the bank insists that the spouses of shareholders sign the statement too. This surprised me because I had assumed that if the company shares are not part of our BSM, no consent for guaranteeing the company’s debt should be necessary. I have separate assets that are not part of our BSM, and I am concerned that by signing the statement of guarantee together with my wife, I might end up guaranteeing the company’s debts with my separate assets—something I definitely wish to avoid. So, my question is: If I sign the statement of guarantee together with my wife, am I also liable with my separate assets?

The answer to your question depends on the specific terms of the document you are signing. If you sign the statement of guarantee as a co-guarantor—meaning the document explicitly identifies you, alongside your wife, as a guarantor—then you will indeed become a co-guarantor. This means you will be personally liable for the debt with all your assets, regardless of whether the company shares are part of the joint ownership of spouses or not.

However, it is more likely that the bank is not asking you to become a co-guarantor, but rather to sign as the spouse of the guarantor. This is an important distinction. Banks typically require a spouse’s consent for legal acts that could potentially affect joint ownership of spouses. This requirement stems from Section 145(1) of the Slovak Civil Code, which states that while each spouse can manage ordinary matters related to joint ownership of spouses independently, for other matters, the consent of both spouses is necessary. Without such consent, the legal act can be deemed invalid.

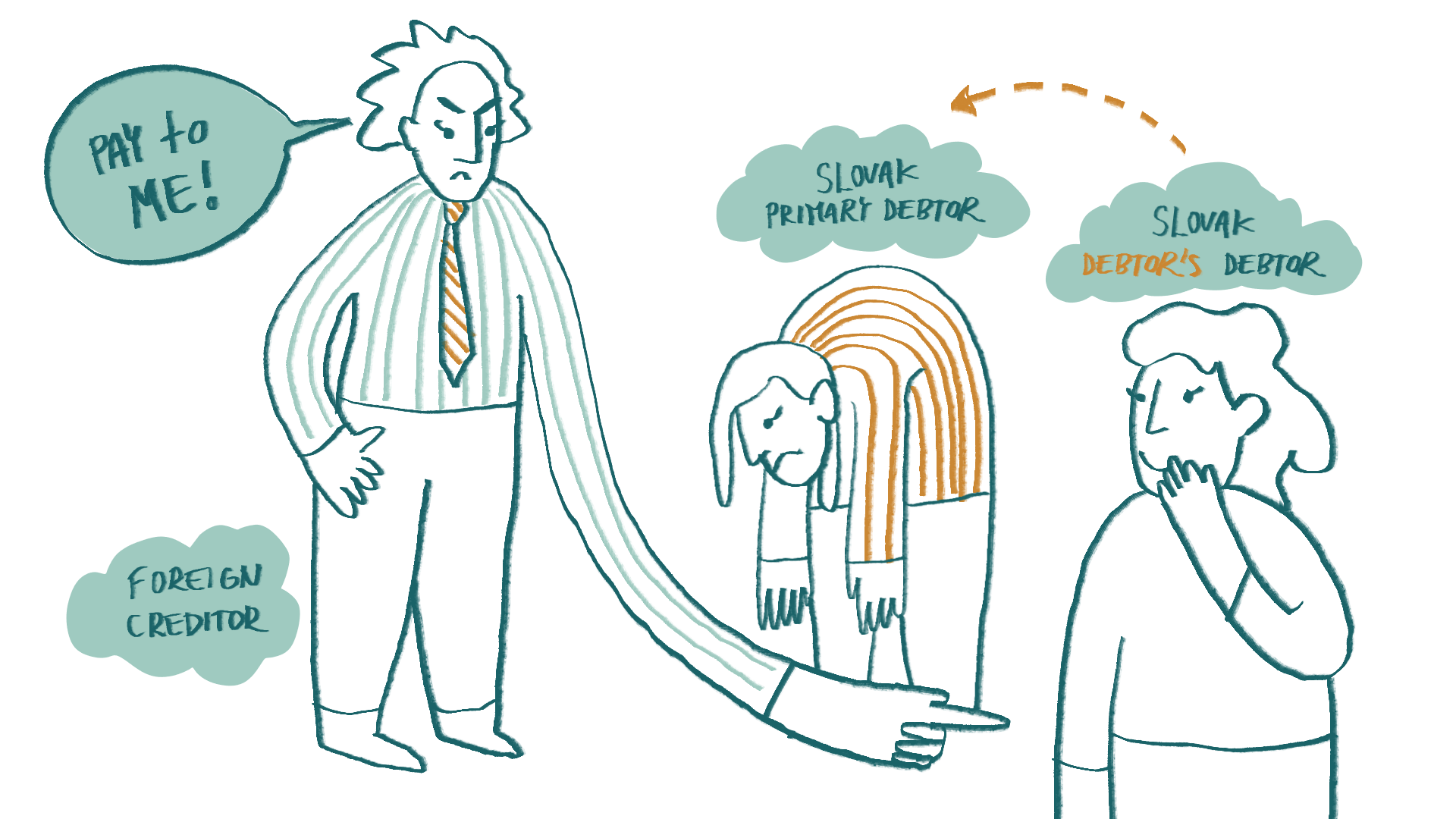

You might argue that since the company shares are not part of the joint ownership of spouses, there is no need for spousal consent for transactions related to such company shares. However, Section 147(1) of the Civil Code provides that a creditor of one spouse can enforce a claim, arising during the marriage, against joint ownership of spouses. In other words, even if your wife’s liability as a guarantor concerns a company not included in the joint ownership of spouses, the bank could still seek repayment from your joint ownership of spouses in case of default.

Banks therefore typically require the consent of the other spouse as a precaution, even in cases like yours, where the legal act involves property that does not fall under the joint ownership of spouses, but in the event of the bank enforcing its claim, assets that are part of the joint ownership of spouses could potentially be used to satisfy the debt. This practice of banks likely stems from an earlier ruling of the Slovak Constitutional Court (I. ÚS 26/2010 of December 8, 2010), which determined that a legal act by one spouse is considered to involve shared assets whenever, the other spouse “ as a result of effects of such legal act, may be deprived of co-ownership of their property in the process of execution.” This ruling introduced an expansive interpretation of which acts require the consent of the other spouse. This broad interpretation has caused banks to raise their cautiousness, leading them to request spousal consent even in situations where it may not be strictly necessary.

The fact that the consent of the other spouse is not necessary when a statement of guarantee is issued by only one of them was confirmed in a later decision by the Supreme Court of the Slovak Republic (1Cdo 27/2017 of May 27, 2020). This decision established that legal acts concerning shared property should only be considered as such if they involve disposition or management of joint marital assets. The Supreme Court stated in this decision that the validity of a legal act whereby one spouse assumes guarantee (regardless of the high value of the obligation) does not require the consent of the other spouse under Section 145(1) of the Civil Code.

So, if the bank requires your signature on the statement of guarantee solely as a form of consent (i.e., not as a direct guarantor but only as the spouse of the guarantor), it is first important to note that this may not be necessary. Your signature will have no effect on the validity of your wife’s surety obligation. However, if the guarantee is enforced and proceeds to execution, the bank’s executor will have the right to seize assets included in your and your wife’s joint marital assets, but not assets that are exclusively your separate property.

If you choose to comply with the bank’s request and sign the statement of guarantee as a form of consent to your wife issuing it, essentially nothing changes. The bank will already have the right to seize assets within your joint ownership of spouses in the event of default on the guarantee obligation. It will not, however, have the right to seize assets that are exclusively your separate property. This is because, by consenting to your wife’s statement of guarantee, you do not become a guarantor yourself. You are merely acknowledging that she has assumed the role of guarantor, and you are aware that in the event of enforcement, the bank may claim assets included in your joint ownership of souses. Therefore, in our opinion, you may sign the statement of guarantee, but only as a sign of consent that your wife has taken on the guarantee obligation.